The attention of the ULSD market turns to Europe, as regional strength attracts arbs

The Red Sea once again maintains its position as the primary source of ULSD resupply into ARA and the MED, if we do not consider the limited supply coming from EC Canada. With European sales prices having increased sharply over the past week, indicating that there is some tightness in the market of late, the arb from the Red Sea into Europe has opened for the remainder of 2023.

Here we see the effect of the closure of USGC arb, and AG/WCI arbs having pointed to the EoS, over the last few weeks.

When discussing signs of European tightness, it is important to once again note the ongoing Russian sanctions, which previously served as Europe’s typical ULSD resupply. Earlier articles have highlighted the redirection of Russian barrels to the AG, LatAm, and WAF.

The relative strength of the European market has widened the E/W ULSD over the past week, with the July E/W ULSD moving from -14 to -17. This trend is expected to continue in the coming weeks, with the earlier mentioned tightness in the European market, and European cracks having reached their highest level since early May.

Additionally, in a further sign of European strength, the MED ULSD Diff has doubled to over 10 USD/MT since mid-May, prompting the opening of the arb from ARA, with the MR VS Leia booked to undertake this route soon.

The Singapore side of the E/W equation is also currently feeling the effect of the Front Tyne VLCC, loaded with ULSD from the AG, which our in-house Pricing Analyst Thomas Cho reports is currently discharging in Singapore and Malaysia.

The USGC continues to serve as the primary source of ULSD resupply for Northern Brazil. However, it faces significant competition from grey Russian sanctioned ULSD barrels, as we previously discussed in earlier articles.

In Southern Brazil, the situation is more mixed, with WCI and AG barrels currently offering the most cost-effective options. The currently lower LR1 AG/WCI to Brazil freights have played a significant role here, reaching their lowest level this year.

Argentina relies on AG barrels as the most cost-effective option currently, while in the WCSAM region, the Far-East has regained its usual primacy. Despite ongoing maintenance in the region, Far-East to Chile MR freights have done a significant amount of the work here, hitting their lowest level this year.

Despite several closed arbitrage opportunities, there has been a surprising increase in HO cracks and spreads over the past week. This suggests that the US may not need to export as much ULSD as normal currently, given that current diesel stocks are towards the lower end of their 5-year seasonal range.

However, US cracks at the front remain negative, while European and Asian cracks are positive. This indicates that the weakness in the global distillate market primarily lies in the US, which aligns with their current diesel demand levels on the back of the current recessionary worries.

Considering the US weakness and European tightness as the main factors, it is expected that the HOGO will continue its widening trend from the past week, working to open the arbitrage opportunity into Europe in the short to medium term, offering some further relief to the US ULSD market.

WCI maintains its dominance as the primary source of ULSD supply into Singapore, a trend observed in recent weeks. Despite falling sales prices, the arbitrage opportunity from WCI to Singapore remains enticing and is expected to remain open for the remainder of 2023.

Freight rates have played a supportive role in this scenario, highlighting a broader weakness in the global freight market.

Here also we have noted a large number of fixtures from India to Australia. Australian strength having added support to the regional prices of late.

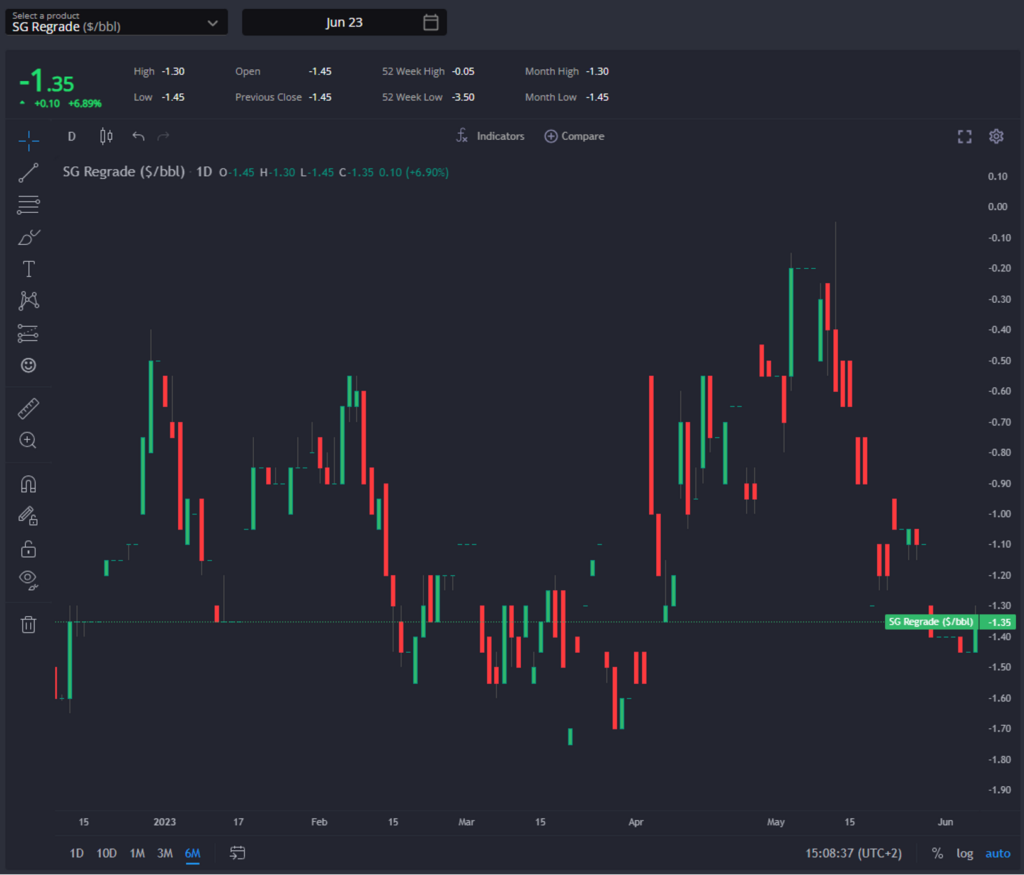

The recent decline in sales prices in Singapore reflects the continued rise in regional stock levels, these again surpassing the previous one-month high recorded last week. However, it should be noted that the Singapore regrade is at its lowest level since March, indicating that a sizeable portion of the inventory build-up might be attributed to jet fuel.

Additionally, the pressure exerted by the earlier mentioned Front Tyne should be considered. As regional maintenance activities are set to conclude by the end of June, the shift in arbitrage patterns from WCI and AG towards Europe is expected to continue. This realignment is likely to result in a widening of the E/W, indicating the market’s anticipation of increased ULSD flows from the East to the West.

[hubspot type=cta portal=7807592 id=38c8d3f4-d2d3-4781-a4a2-ba10ca4055bc]

James Noel-Beswick is Commodity Owner for Sparta. Before joining Sparta, James worked as an analyst for likes of BP and Shell, and leads our continued development of the distillate product vertical.

Sparta is a live, pre trade analytics platform that enables oil traders, refiners, banks, hedge funds and wholesalers to have access to real-time and global actionable insights to capture market opportunities before others.

To find out how Sparta can allow you to make smarter trading decisions, faster, contact us for a demonstration at sales@spartacommodites.com

Similar articles

Book a demo to see how Sparta enables you to trade with conviction